I’ve watched this assumption persist for years. China copies, scales what works, and struggles to innovate. The data no longer supports that view. In 2025, Chinese technology entered the World Intellectual Property Organization’s (WIPO) Global Innovation Index (GII) top 10 for the first time.

What matters more than the ranking is the shift it confirms. China’s technology sector has moved from adapting foreign models to building original ones. The question is not whether technology from China will reach global markets. It is whether businesses are paying attention before it arrives.

China Ranked in the Global Innovation Top 10 for the First Time in 2025

In September 2025, WIPO ranked China 10th globally in its annual GII. It was the first time the country entered the top 10. China also held 24 of the world’s top 100 innovation clusters. The Shenzhen-Hong Kong-Guangzhou cluster ranked first globally for the first time.

The GII measures 139 economies across seven pillars, including:

- Institutions

- Human capital

- Infrastructure

- Market sophistication

- Business sophistication

- Knowledge outputs

- Creative outputs

China’s position ahead of France, the Netherlands, and Israel on this measure is not the result of a single policy push. It reflects a structural change in how Chinese companies build.

For most of the past two decades, the dominant narrative held that China’s companies execute fast but originate slowly. That narrative has weakened.

China’s advanced technology sectors now lead globally in solar manufacturing, high-speed rail, electric vehicles (EVs), unmanned aerial vehicles (UAVs), and graphene. In each area, the leadership came through a cycle of intense domestic competition, rapid iteration, and scale.

These sectors share a common thread. None of them reached global leadership through government direction alone. They succeeded because private companies competed fiercely in a market that offered no protection for slow movers. That competitive intensity is what produces the iteration speed that observers outside China consistently underestimate.

The Platform Ecosystem Is the Product, Not the App

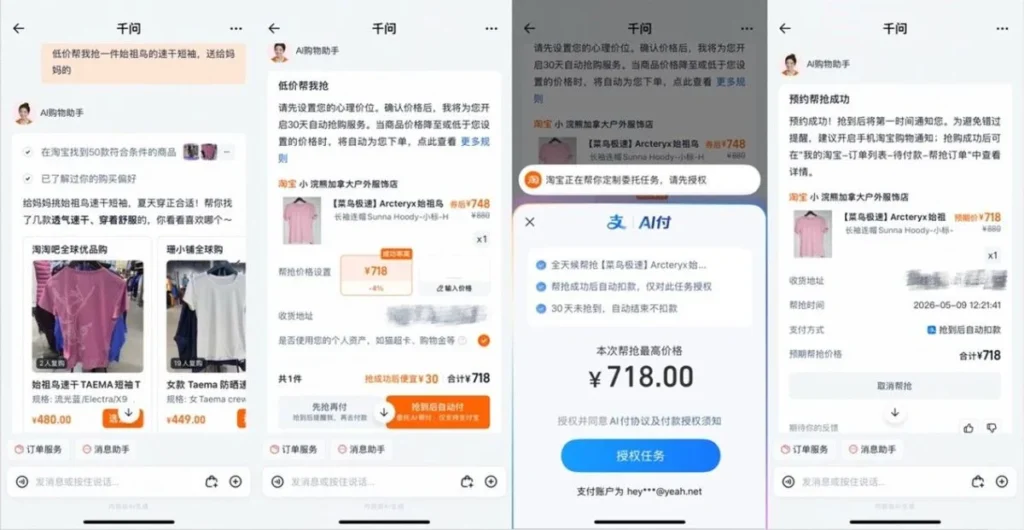

WeChat (微信) launched in 2011 as a messaging app. By April 2026, it had 1.4 billion monthly active users and functioned as operational infrastructure for daily life in China. Payments, healthcare appointments, government services, transport, and commerce all run inside a single application.

What WeChat offers brands is the architecture itself. Merchants build mini programs, sub-applications inside WeChat, instead of investing in standalone apps. They skip the friction of external downloads, separate payment systems, and independent customer service channels. Everything connects inside a closed loop.

That closed loop changes the economics of customer access. A brand that builds inside WeChat reaches users where they already spend their digital time. No redirection cost. No separate acquisition channel.

In China, social commerce and payment infrastructure were built as a single system from the outset. Other markets added them separately. That difference shows most clearly when a company tries to expand into adjacent services and discovers that each new addition requires a new integration point.

Western platforms are studying this model. Elon Musk has stated that his ambition for X, formerly Twitter, is to become an “everything app.” Efforts to build super apps outside Asia have repeatedly stalled. Regulatory environments and fragmented payment infrastructure in the United States and Europe make the model structurally difficult to replicate.

Live Commerce Moved from China’s Fringe to the Global Standard

Live commerce in China started with skeptics. Early Western analysis treated it as a behavior specific to Chinese consumers, shaped by mobile-first habits and integrated payment systems.

According to the China Internet Network Information Center (CNNIC) 56th Statistical Report, 976 million people in China shopped online as of June 2025. That represents 86.9 percent of all internet users. A significant share of those purchases flows through live commerce platforms. Douyin (抖音) and Taobao Live demonstrated that real-time entertainment merged with commerce generates higher conversion rates and faster purchase decisions than static product pages.

The format is now a global category. Amazon, Instagram, and YouTube have each built live shopping features. Each cites Chinese market benchmarks when explaining the strategic rationale.

China’s tech advances in live commerce and social retail consistently run three to five years ahead of Western adoption. In-store automation and retail technology in China follow the same pattern.

Companies tracking live commerce in China today are watching the next stage of global retail form in real time. The adoption patterns are visible. The timing is the variable.

The lag between Chinese live commerce adoption and Western adoption is predictable. It is also shrinking.

Alipay and Cainiao Rewrote What Logistics and Fintech Infrastructure Means

China’s approach to payments illustrates what infrastructure sequencing produces. The country had low credit card penetration when smartphones arrived.

Chinese fintech companies built QR (quick response) code-based systems directly rather than a card-based layer first. China moved to near-cashless commerce faster than economies with established card infrastructure to work around.

Alipay (支付宝), developed by Ant Group, is the largest example. It began as a checkout tool for Taobao purchases and expanded into:

- Wealth management

- Insurance

- Microlending

- Municipal payments

Countries across Southeast Asia have since adopted QR payment frameworks built on the Chinese model, adapting the architecture to local regulatory conditions.

Cainiao, Alibaba Group’s logistics arm, followed the same infrastructure-first logic. As of July 2025, Cainiao operates warehousing and fulfillment across 10 Asia-Pacific (APAC) markets with a same-day outbound rate of 99.9 percent.

Its stated goal is worldwide delivery within 72 hours. Cainiao operates more than 40 overseas warehouses across Europe, North America, and the APAC region.

The strategic point is sequencing. Cainiao built the infrastructure before the volume arrived. That approach avoids the margin pressure that hits logistics operators who scale capacity reactively. Alipay followed the same logic. The architecture came before the use cases, which is why both platforms absorbed new services without rebuilding from the base.

How Chinese Tech Companies Replicate Models Across Markets

Chinese technology companies operate with a specific expansion logic. They validate operating models at scale in China’s intensely competitive domestic market. Then they move those models into international markets where competition is less acute.

Xiaohongshu (小红书), also known as Red, built a content-commerce model in China that blends user-generated content, short video, and in-app purchasing. ByteDance launched Lemon8 internationally using the same architecture.

This cross-market replication is deliberate. The model was already proven at scale. What changed was the geography.

I’ve watched this pattern play out across multiple sectors. Companies with direct exposure to China’s technology market tend to treat it as a three-to-five-year signal for global consumer behavior, rather than as an isolated case study. That framing consistently produces better decisions.

BYD’s (Build Your Dreams) vehicle export trajectory illustrates the same logic in manufacturing.

The company refined production processes, battery technology, and pricing in China’s domestic EV market at volumes no other manufacturer could match. It then expanded globally with cost structures and iteration speeds that established players were not prepared for.

The sequence is consistent across sectors. Technology from China travels outward as a system export, carrying operating logic and not just product features. Companies tracking China’s technology trajectory are watching global diffusion play out at a delay. That delay is shortening.

What Executives Need to Know Before China’s Technology Models Become Standard

Three observations stand out for global leaders.

First, track the operating model, not the product name. WeChat became dominant by building a payment and commerce layer that made leaving the platform costly for users. Executives who studied the app missed the architecture underneath it. Those who studied the architecture understood where value would accumulate.

Second, live commerce, social retail, and QR payment adoption outside China are following the same adoption patterns visible inside it, offset by a few years. Teams that understand consumer behavior patterns in China today have a verifiable head start on what their own markets will require next.

Third, infrastructure sequencing has long-term competitive consequences. Chinese companies that built logistics and payment infrastructure before scaling their user bases ended up with structurally lower costs. That was a deliberate choice, not an accident of scale.

Understanding China’s AI strategy belongs in the same frame. China’s technology advancement in artificial intelligence (AI) follows an infrastructure-first approach. The same pattern that proved itself in payments and logistics is now repeating in AI.

What Does China’s Technology Shift Mean for Your Business Strategy?

As China’s technology models move from domestic test bed to global template, executive teams face a sharper question. How do you act on what China signals before it becomes the standard everyone is reacting to?

Ashley Dudarenok works with global teams to translate China’s technology advances into sharper strategy, stronger market positioning, and more grounded operational decisions.

She helps brands understand how China’s operating models in commerce, payments, and platform design are redefining consumer expectations across global markets.

Invite Ashley Dudarenok to speak on what technology from China signals for global business. Her sessions give leadership teams a concrete view of what these models mean for their sector and their next strategic cycle.

Quick Answers on Technology from China and Global Diffusion

Below are key answers to recurring questions about how Chinese technology spreads, what operating conditions enable it, and what global companies should watch.

What Is Technology from China Most Recognized for Globally?

Technology from China is recognized for mobile payments, live commerce, electric vehicles, and platform models that bundle multiple services into one user experience.

How Does Chinese Technology Development Differ from the Western Approach?

The key difference is sequencing. Chinese companies build infrastructure first and scale products on top. That approach produces lower costs and faster expansion.

What Does “Platform Ecosystem” Mean in the Context of Chinese Technology?

In Chinese technology, a platform ecosystem is a single application hosting payments, commerce, and services together. Users complete transactions without leaving the platform.

Which Chinese Technology Companies Are Most Active in Global Expansion?

DJI leads globally in commercial drones. Huawei supplies telecoms infrastructure across Africa and Asia. Shein has changed fast commerce dynamics in North America and Europe.

How Do China’s Technology Adoption Patterns Differ from Markets in Europe or North America?

China’s adoption is faster. Intense competition and a large mobile-first consumer base prove formats quickly. Western markets typically follow several years later.

What Is Infrastructure Thinking and Why Does It Matter for Global Executives?

Infrastructure thinking means building payments, logistics, and data systems before scaling user-facing products. Companies that sequence this way carry lower costs at scale.

How Does Business Model Transfer from China to Overseas Markets Actually Work?

Chinese companies enter new markets with models proven under intense domestic competition. They adapt pricing and compliance locally but keep the core operating architecture unchanged.

What Scale Effects Make Chinese Platform Models Difficult to Replicate?

Chinese platforms generate feedback loops from large user volumes. Those loops improve targeting and logistics faster than smaller markets allow, creating a growing performance advantage.

What Has Changed Most in China’s Technology Advancement Since 2020?

The biggest shift is that Chinese technology companies now define performance benchmarks in several technology categories, rather than working toward benchmarks set by others.

What Are Clear Examples of Cross-Market Replication from China Beyond Electric Vehicles?

Chinese group-buying formats pioneered by Pinduoduo are active across platforms in Indonesia, Brazil, and India. Chinese supply chain software is spreading through Southeast Asian manufacturing.

What Industry Signals Should Executives Track to Stay Ahead of China’s Tech Advances?

Watch which formats drive repeat purchases among young Chinese consumers. Those formats typically appear in Southeast Asia within two years and Western markets within five.

How Does Ecosystem Integration in Chinese Platforms Differ from Western Platform Design?

Chinese platforms treat payments, content, and commerce as one integrated experience. Western platforms build these as separate layers, adding friction where services connect.